The Super Strategy Most Accountants Never Mention: Spouse Contribution Splitting

If you've got a spouse whose super balance is a lot lower than yours, there's a strategy sitting right under most people's noses that almost never gets raised at tax time. It's called spouse contribution splitting, and it lets you move up to 85% of last year's concessional contributions into your spouse's super account.

It's not a loophole. It's a completely legitimate ATO-sanctioned strategy. It's just widely under-used, mostly because it requires a bit of forward planning and isn't something that happens automatically. Let's walk through what it is, why it matters, and why so many accountants never bring it up.

What Is Spouse Contribution Splitting?

Spouse contribution splitting allows a super fund member to transfer a portion of their concessional contributions (employer contributions, salary sacrifice, and personal deductible contributions) from one financial year into their spouse's super account, in the following financial year.

The key details:

You can split up to 85% of your concessional contributions - the remaining 15% accounts for the contributions tax already paid inside the fund

The split applies to contributions made in the previous financial year - you can't split contributions from the current year

The application must be lodged with your fund (or, for an SMSF, documented and processed correctly) generally by 30 June of the following financial year, or earlier if you're rolling over or starting a pension

Only concessional contributions can be split - non-concessional (after-tax) contributions aren't eligible

Example: If you have $30k of employer contributions in the 2025-26 financial year, you could apply in the 2026-27 financial year to split up to $25,500 (85%) of that into your spouse's super account.

Why This Strategy Actually Matters

On the surface, splitting contributions might just look like moving money from one pocket to another. But the flow-on effects can be significant.

1. Equalising Super Balances Between Spouses

Many couples end up with a large gap in super balances - often because one partner took time out of the workforce, worked part-time, or earns significantly less. Splitting contributions helps close that gap over time, which matters for a few reasons:

It allows both spouses to make better use of their own transfer balance cap (the amount each person can move into a tax-free pension account)

It can help both spouses access catch-up concessional contribution opportunities more evenly

It reduces the risk of one spouse being "capped out" on contribution strategies while the other has years of unused capacity

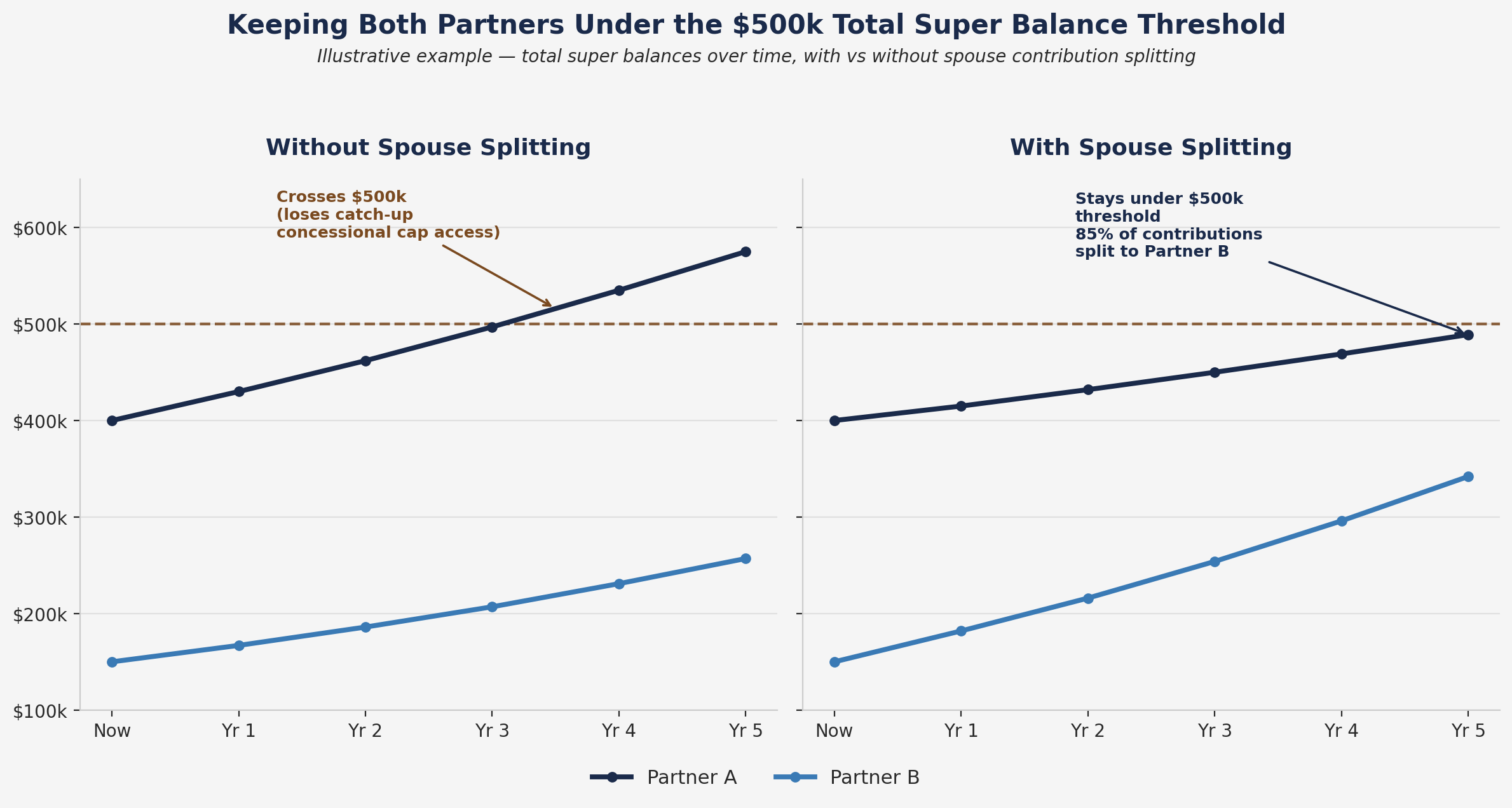

2. Managing the Total Super Balance Thresholds

Your total super balance at 30 June each year determines what you're allowed to do the following year - things like whether you can make non-concessional contributions, use the bring-forward rule, or access catch-up concessional contributions.

If one spouse is approaching a total super balance threshold and the other has plenty of room, splitting contributions can help keep both balances in a more favourable position, opening up contribution strategies that might otherwise be lost.

3. Age-Based Access and Retirement Timing

If there's an age gap between spouses, splitting can help the older spouse build their balance faster so they can access pension phase (and its tax-free earnings) sooner, rather than waiting for the younger spouse's balance to catch up naturally.

4. Asset Protection and Estate Planning

Spreading super more evenly between spouses can also support broader estate planning and asset protection goals, particularly where one spouse has higher professional or business risk exposure.

Why Most Accountants Miss This

This strategy isn't complicated once you understand it, but it rarely comes up in a standard tax return conversation. Here's why:

It requires proactive planning, not just compliance. Most tax return preparation is backward-looking - accountants are focused on lodging what's already happened, not restructuring contributions for next year.

The timing is easy to miss. Because you're splitting last year's contributions, it's easy for the window to close before anyone thinks to raise it.

It only applies to concessional contributions. If a client's contributions are mostly non-concessional, or if nobody's tracking contribution types by category, the opportunity can slip through unnoticed.

It requires looking at both spouses' super together. Most tax return preparation happens on an individual basis, so a strategy that only makes sense when you look at the household as a whole is easy to overlook.

There's no compliance risk in not doing it. Nothing goes wrong if you skip it - which means it's rarely flagged as urgent, even though the value compounds every year it's missed.

Important Considerations

Spouse contribution splitting isn't right for every couple, and there are some eligibility rules to be aware of:

The receiving spouse must be under their preservation age, or between preservation age and 65 and not yet retired

The receiving spouse cannot already be in retirement phase drawing a pension from that split amount

Splitting doesn't reduce your own contribution caps - the contribution still counts against the contributing spouse's concessional cap in the year it was made

It only moves contributions between spouses - it doesn't create any additional tax deduction or contribution room

Paperwork and timing matter, so it needs to be properly documented and lodged within the required window

The Bottom Line

Spouse contribution splitting won't suit every couple, but where there's a meaningful gap in super balances, it can be a genuinely valuable, no-cost strategy that's often overlooked simply because it requires someone to actually look ahead rather than just look back.

As SMSF Specialist Advisors™, we build this kind of forward planning into our ongoing advice - not just at tax time, but as part of an ongoing conversation about how your super and your spouse's super work together.

If you'd like to find out whether spouse contribution splitting makes sense for your situation, we'd love to chat.

Disclaimer: This article provides general information only and does not constitute personal financial advice. Superannuation rules are complex and subject to change. You should seek professional advice tailored to your specific circumstances before making any decisions regarding contribution splitting or your SMSF.